My Childhood Friend's E-Stamp Business Beats My Stock Portfolio 6:1

"I thought proximity to information mattered. But proximity to cashflow matters more."

Two years of investing “smartly” vs. one conversation over chai in my hometown

“Six percent per month?” I repeated, thinking I’d misheard.

“Per month,” Rakesh confirmed, stirring his chai.

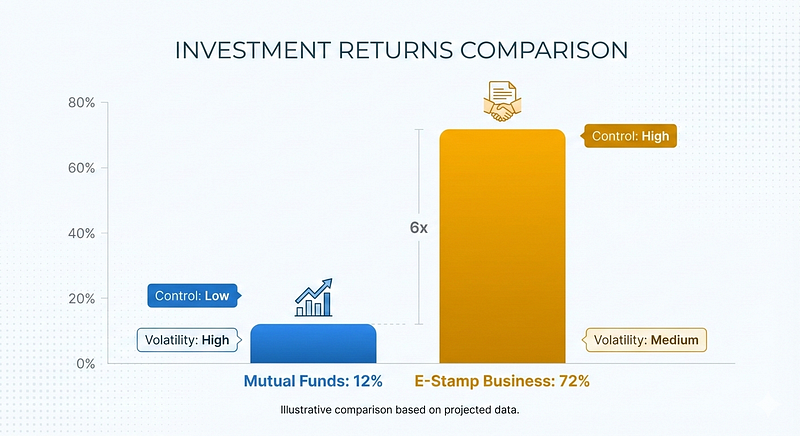

I had a Computer Science degree, three years of “smart” investing, and a diversified portfolio returning 12% annually. My childhood friend ran an e-stamp shop in Lucknow. Yet somehow, his numbers made mine look like a rounding error.

I actually laughed. “You mean per year, right? Even that’s less than FDs these days.”

He looked at me like I was the one being slow. “Bhai, per month. 6% per month.”

That conversation was two months ago. It’s changed how I think about money completely.

How We Got Here

Let me rewind a bit.

I’m a software engineer — B.Tech in Computer Science, decent college, the whole package. Always been the planning type. The kind of person who color-codes spreadsheets and tracks every rupee. Introvert, perfectionist, you know the type.

My financial philosophy was textbook diversification: stocks, mutual funds, crypto (yeah, I went there), gold, bonds, some side projects in software. Whatever I could manage alone, because talking to people about money felt… uncomfortable.

After three years of this, my portfolio was averaging around 12% per annum. On paper, respectable. In reality? It barely covered my monthly bills, let alone gave me any real freedom.

Rakesh and I grew up together in Lucknow. He was the opposite of me in school — average grades, super extroverted, the guy who knew everyone’s cousin’s friend. Street smart in ways I never was. He didn’t get into a top college, did his graduation locally.

While I was climbing the corporate ladder outside our hometown, he started an e-stamp business two years ago. Got inspired by a successful local vendor, got his government license, and just… started.

The Conversation That Changed Everything

I visited home during Diwali last year — first time in months. We caught up over chai at his small office near the registry office. The place smelled like printer ink and had that constant hum of the old HP machine churning out stamps.

I told him I was doing okay job-wise, but honestly frustrated with my investments. Everything felt slow, unpredictable, or straight-up disappointing.

“What about you?” I asked. “How’s the stamp business?”

“It’s good,” he said. “Actually, it’s growing faster than I expected. Problem is, I need more liquidity.”

See, e-stamps are basically digital stamp papers for legal documents — property registrations, agreements, affidavits. In Uttar Pradesh, especially in the capital, property transactions never stop. People need stamps, and they need them fast.

“How much do you need?” I asked, half-curious.

“Minimum one lakh. Maximum whatever you’re comfortable with. I can give you 6% per month.”

That’s when I laughed and said the FD thing.

His response stopped me cold. “Not per year. Per month.”

I did the math in my head. 6% per month is 72% per year. My mutual funds suddenly felt like a bad joke.

How This Actually Works (And Why I Didn’t Immediately Think It Was a Scam)

First instinct? Google “e-stamp business scam” the moment I got back to my room. I’m not stupid.

But here’s the thing — the economics actually make sense.

Rakesh holds a government-issued license to sell e-stamps. He’s registered, operates from verified premises, the whole thing is legit. Each stamp he sells, he earns about 1.5–2% commission from the government.

“But how does 1.5% turn into 6% for me?” I asked him the next day.

“Volume and velocity,” he explained. “Say someone’s buying a property worth ₹50 lakhs. They need a stamp for the registry. That’s one transaction, I make my cut. But that same capital? It rotates through 15–20 customers in a month. Small margins, but the money moves constantly.”

He showed me his transaction register. During wedding season and year-end, he was doing 20+ stamps a month. Even in slow months, it was 10–12. The math checked out.

The reason he needs external capital? He currently operates with about ₹20 lakhs total. If he had more liquidity, he could handle bigger customers — builders, property dealers, legal firms. Right now, he sometimes has to turn people away during busy periods.

“Why not just take a business loan then?” I asked. “Banks would give you 12–15%.”

He made a face. “Loans come with headaches. Documentation, pressure, EMIs even if business is slow. You’re my friend. If I can’t pay you one month, you’ll understand. Bank won’t.”

Fair point.

The Decision (And My Parents’ Reactions)

I didn’t jump in immediately. Thought about it for three days.

Called my parents. Dad said, “Rakesh is a good boy, but this seems too good.” Mom said, “What if something happens to him?” Both valid concerns that I didn’t have great answers to.

Here’s what I decided: I’d invest ₹2 lakhs. Not life-changing money, but enough to test this properly. I insisted on monthly payouts, no excuses, and told him we’d formalize everything in writing once I saw it working.

He agreed.

That was two months ago. He’s paid 6% both months, on time. ₹12,000 each month, transferred directly to my account.

I still refresh my mutual fund app more than I’d like to admit. Old habits.

The Math That Made Me Rethink Everything

Let’s be honest about the numbers:

- My mutual funds: ~12% per year, subject to market mood swings, zero control

- Rakesh’s business: 6% per month = ~72% per year (if it continues), actual cashflow I can see

The difference isn’t intelligence or some secret strategy. It’s positioning.

I was fighting for scraps in a market dominated by institutional players, trying to time entries and exits, reading analyst reports. Rakesh just knows when Mrs. Gupta needs a property stamp by Friday, and he makes sure he can deliver it.

This is what I got wrong: I thought proximity to information mattered — Bloomberg terminal access, market news, technical analysis. But proximity to cashflow matters more. Rakesh doesn’t know what “alpha” means. He just knows his customers.

Why Millionaires Keep Working (I Think I Get It Now)

You know what’s funny? I used to wonder why founders of successful companies keep working 60-hour weeks even after they’re worth hundreds of crores.

Now I think I understand.

Operating cashflow — the actual movement of money through a business you control — compounds faster than passive ownership ever will. When you’re just investing in stocks, you’re betting on someone else’s execution. When you’re close to the business, you are the execution.

That’s why they don’t just “retire and invest in index funds.” They’re not working because they need money. They’re working because that’s where the real money is made.

Let’s Talk About the Risks (Because This Isn’t Free Money)

Okay, reality check time.

This is not a guaranteed 72% forever. Here’s what keeps me up at night:

Business Risk:

- Property market slows down → fewer transactions

- Government policy changes → commission structures change

- Festive seasons are great, but summers are slower

- Competition increases in Lucknow

Personal Risk:

- What if Rakesh gets sick or has personal issues?

- What if he decides to expand into unrelated businesses I don’t understand?

- What if our friendship gets weird over money?

Capital Risk:

- This money is illiquid. I can’t just “withdraw” it like from a mutual fund

- It’s a concentrated bet on one business, one person, one city

- No SEBI protection, no formal grievance mechanism (yet)

The Uncomfortable Truth: If this were genuinely guaranteed money with zero risk, institutional investors would’ve already dominated this space. The fact they haven’t tells you something. Small businesses like this exist in inefficient pockets of the economy — high returns, but also high friction, relationship-dependent, and hard to scale.

My plan moving forward: I’ll scale up to ₹10 lakhs maximum (not ₹50 lakhs, because I’d never put all my eggs in one basket), but only after:

- A proper written agreement with clear terms

- At least 6 months of consistent payouts

- A realistic floor of 4% per month to account for slow periods

The Red Flags I’m Watching For

I’m not naive about this. Here’s what would make me pull out immediately:

- If he starts delaying payments or asking for “patience”

- If transaction volume claims don’t match actual payouts

- If he suddenly wants to expand into unrelated businesses

- If he resists formalizing our agreement in writing

- If other “investors” suddenly appear that I don’t know about

So far, none of these have happened. But I’m watching.

Why I’m Not Putting ₹50 Lakhs In (Even Though the Returns Are Crazy)

People might wonder: “If it’s so good, why not go all-in?”

Simple. I could never rely on a single source, no matter how good the returns look. Whether it’s 12% or 72%, putting all your money in one place is just asking for trouble.

I also have emergency savings in FDs that I’ll never touch unless everything else fails. Diversification isn’t just about asset classes — it’s about risk types.

The moment this becomes my only source of investment income, I lose objectivity. I need to stay rational, not desperate.

What This Means for You (And Me)

I’m not saying everyone should invest in their friend’s business. That’d be stupid advice.

But here’s what I am saying:

We’re often optimizing the wrong variables.

We chase information when we should be chasing proximity. We read about wealth creation when we should be talking to the people who actually handle cashflow daily.

The opportunities aren’t always on your Zerodha app or in your Twitter feed. Sometimes they’re in your hometown, run by people you’ve known for years, doing unglamorous work that actually matters.

I don’t know if this will work long-term. I’m two months in, not two years. Maybe next year I’ll write a follow-up titled “How My Friend’s Business Collapsed and I Lost ₹10 Lakhs.” That’s possible.

But I do know my perspective has shifted.

The Question I Keep Asking Myself

How many of us are reading the same newsletters, watching the same YouTube gurus, investing in the same stocks — and wondering why we’re not getting ahead?

Meanwhile, there’s probably someone in your network who’s quietly building something real. Not glamorous, not trending on Twitter, but generating actual cashflow.

What would happen if you had that conversation?

Not to invest blindly. But to learn. To understand. To see money from a different angle.

Because here’s the truth: there’s no easy money. My 72% comes with risk, uncertainty, and relationship management. My 12% mutual funds come with market volatility and zero control. Pick your hard.

But at least know what the options are.

Final Thought

I’ll update this in a few months — honestly, whether it goes well or badly. Because the real lesson isn’t about e-stamps or small businesses. It’s about questioning the default path.

We’re all told to “diversify,” “invest long-term,” “trust the process.” That’s not wrong. But it’s incomplete.

Sometimes the smartest investment is the one that doesn’t fit in a neat category.

If this resonated, I’d genuinely love to hear your experience. Have you invested in a friend’s business? How did it go? What did you learn?

Drop a response in comment. Finance is for everyone, but understanding money requires stepping outside the obvious.